Written by Fernando Martin| March 11, 2019

Written by Fernando Martin| March 11, 2019

There are many people from all walks of life that are commercial real estate investors�small business owners, corporate executives, professional service providers, entrepreneurs, and professional investors. With the right preparation and understanding, commercial real estate (CRE) is the perfect asset for an investor to earn passive income while owning an appreciating asset. However, commercial real estate is not without its risks, so it�s important that any potential investor understands what they�re getting themselves into. Here are 5 steps to follow in order to jump into the commercial real estate investment game safely:

It�s important to set an affordable budget for the property (either with or without financing) that can withstand any market changes or corrections. Stretching too far or leveraging too much can lead to a seriously precarious position if the economy or real estate market changes, especially if tenants are lost or if there is a refinance that needs to be addressed during that time frame. Can you imagine having to deal with a maturing loan that had maximum leverage during the 2008-2009 credit crunch? It�s one of the major factors that lead to the huge amount of short sales, foreclosures and bankruptcies during the last recession and not a situation that anyone wants to find themselves in.

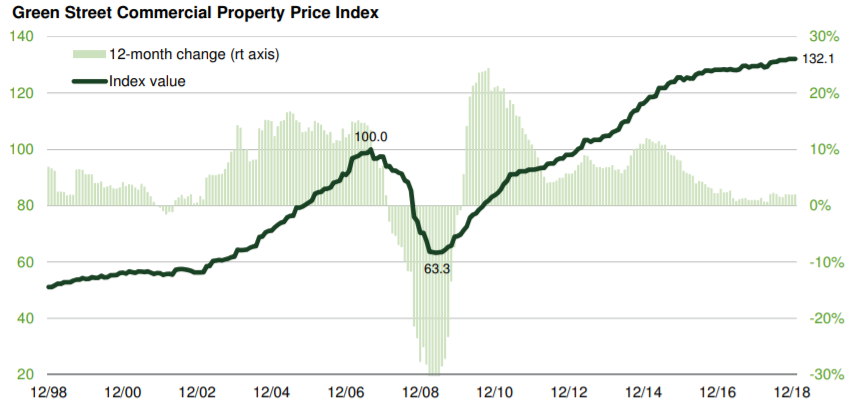

Source: Green Street Advisors.

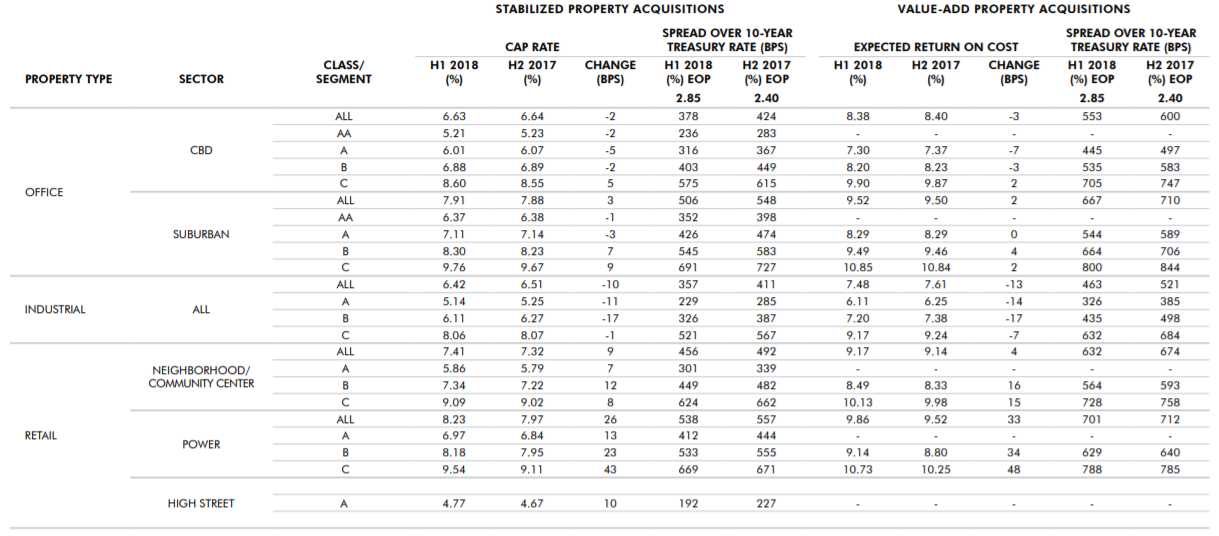

Understand how much money you need to earn (or save) from the property to make it worth while, factoring in acquisition price and potential future sales price. One helpful way to see if an investment property will meet your requirements is to look at the capitalization rate, if it can be easily relied upon. This allows you to see what types of returns you would be making (assuming no debt is used). However, make sure that you are using actual numbers from the property�s financial statements rather than broker projections, which could skew the cap rate to the buyer�s detriment. The higher the capitalization rate, the higher the potential returns, but also the higher the risk profile of the property. Here are the average capitalization rates for US real estate markets as of 7/1/18:

Source: CBRE, Inc.

If you are buying or building a property for your own business, it is important to compare your monthly mortgage payments to what you would otherwise be paying in rent, taking into consideration any potential future rent or interest rate increases (especially when you are on an adjustable rate mortgage) as well as the affordability of the payments for your particular business. Also worth serious consideration is what impact any economic changes or industry cycles could have on your business; in the event business is slow for a period of time, you still need to make sure you can cover your mortgage payments and business expenses without a problem.

Source: The Balance

The market that you decide to invest in should be an area you are very familiar with, ideally somewhere that is within a day�s drive from your primary residence. Perhaps this is an area where you or your family members live, where you went to college, or another location that you�ve spent a significant amount of time. Keep in mind that the further you go from where you currently reside, the more difficult it will be to oversee the operations of the property (even if a property manager is in place), which could potentially lead to an increase in vacancies or deferred maintenance, overpaying for property expenses, under-pricing rents, or other difficulties with the property. Other geographic factors to consider are ability to resale the property, demographics, and population growth trends.

Choosing a commercial property type is easy if you�re buying for your own business because it would be whatever property type is suitable for performing the functions of that business. However, if you are looking for an investment property, it may be a bit trickier depending on how the economy is doing, what the future projections are, and what the demographics and businesses are in the area that you�re considering investing. For instance, office always seems to do well in an area with many professionals and businesses focusing on the tech or service sectors, whereas warehouses typically do better in industrial areas, agricultural areas, or distribution hubs where there is a need for manufacturing, storing equipment, or temporarily holding goods meant for other destinations. Being aware of what types of industry are in the market is exceedingly important to a successful investment strategy.

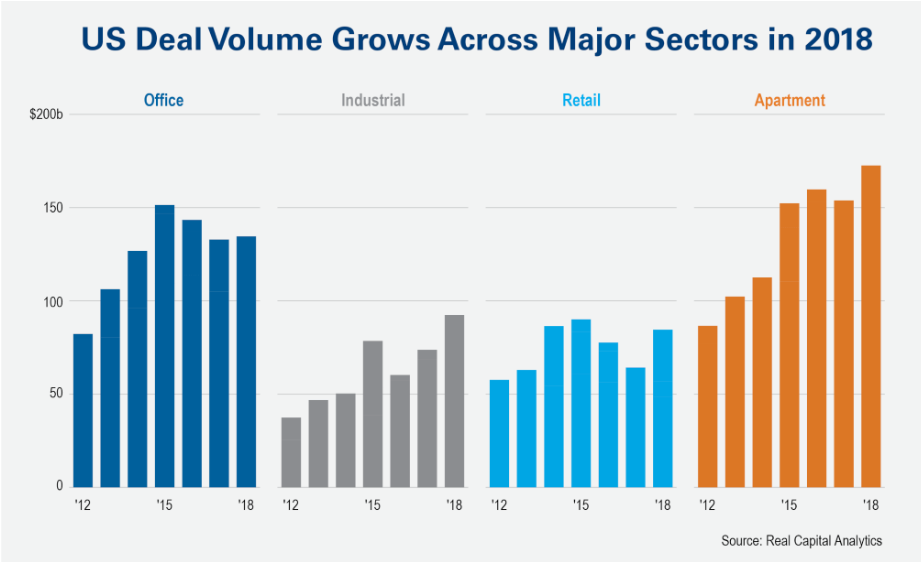

Source: Real Capital Analytics

Identify a property in your chosen market that meets your budget and returns requirements, making sure to avoid any of the typical first-time investor pitfalls. Also, you will want to work with an experienced broker (separate from the selling broker) to help you negotiate the terms of the purchase and sale agreement, including any due diligence or financing contingencies. Things to take into consideration when analyzing a property for potential acquisition are:

Prevailing lease rates and terms; check for concessions like free rent or tenant improvements

Area vacancy rates

Whether property taxes are reassessed after the property sale, which could increase expenses

How the property has performed through past recessions

Length of tenant leases and history of payment (i.e. if they�ve been paying on time)

History of property uses (ask for a Phase I environmental engineering report to check for potential contamination).

Area crime rates

Property visibility from the street

Once you�ve found a property that passes due diligence and meets your financial requirements, it is time to negotiate the terms of the sale with the seller. When you sign your Letter of Intent or Purchase and Sale Agreement, make sure that you give yourself enough time to get comfortable with the property and financials and build in an �out� without losing escrow money in case you find something undesirable during the due diligence period. Additionally, you will probably want to put in a financing contingency in case something comes up during the lender�s underwriting that makes the borrower or property disqualified from receiving financing.

Unless you are purchasing the property in cash or in full through a 1031 exchange, you will need to consider what type of financing you would like to put on the property once it�s under contract. The options available for financing will depend on whether the property is owner-occupied or investment, the financial strength and credit worthiness of the borrower(s), the property type and location, and the property performance. Once you�ve gotten yourself up to speed on the different loan options you can qualify for, you will need to start preparing a financial package and submit a loan application to start the loan qualification process. If you need help determining what you may qualify for, our loan finder is a great place to start:

If you are purchasing the property for your current business or a start-up business (i.e. an owner-occupied property), you may be able to put down as little as 10-20% on the property if you are getting a SBA loan. However, if you are leaning toward a more conventional product (i.e. bank loan), you will probably need at least 20-25% down, with some exceptions made for professionals (doctors, lawyers, CPAs, etc.). Keep in mind that the annual business net income still must be able to cover at least 125% of the annual mortgage payments, also known as a 1.25x debt service coverage ratio. A great way to see if your business can meet that requirement is by testing it on our DSCR calculator.

If you are purchasing an investment property, you should always plan on putting at least 25% down, although some properties may require more, especially if they are specialty use or hospitality, which are considered higher-risk assets. Additionally, with the exception of multifamily, investment properties usually have higher debt service coverage ratios (1.30-1.5x) than owner-occupied properties.

If done correctly, yes. Primarily, investors profit from commercial real estate by collecting the cash flow from the property (if investment), building equity by paying down the principal balance of their loan, and by the property appreciating in value over time. Another way to make money from commercial properties is through speculative development or value-add by re-stabilizing or substantially rehabilitating an existing building. However, that is not an approach we would recommend for new investors as it can be very expensive and extremely risky unless you are already well-reversed in construction and tenanting.

Although a person with any background can become a commercial real estate investor in the right circumstances, the wrong misstep can wipe out any or all of the profitability of a property, so it�s important to pay attention throughout the entire purchasing and financing process. Typical mistakes investors make include over-paying for a property, not verifying leases or financial statements, taking on an asset or market they don�t understand, or being on a loan product poorly suited for their needs.

So this is a tricky question, with an even trickier answer. Can it technically be done in limited circumstances? Yes. Should you be investing in commercial real estate if you can�t already afford it? In most cases, the answer is �no.� This is an industry where it takes money to make money and if you end up finding yourself in a situation where you need additional cash for the property because of emergency repairs or other unforeseen circumstances, you could end up finding yourself in a serious quandary if you can�t come up with the money. That being said, if you want to take the credit risk or can come up with enough money for contingencies, you have a couple of options for purchasing commercial real estate with little to no money currently in your bank account:

Borrow the money from friends or family

Use seller financing

Use a HELOC to pull out funds from your residence

Bring in a partner with money

Do a cash-out refinance of a property you already own

Sell another property or other assets you already own

After taking into consideration your annual cash flows and potential future sales price, if you aren�t going to be able to out-perform the stock market (average annual return of 8.6%), or publicly traded Real Estate Investment Trusts (average annual return of 11.8%), then it�s probably not worth the time, money, risk, or effort.

Fill this form out to find the best commercial loan programs for your needs.

Get a free commercial loan quote. This process does not affect your credit score.

Fernando and Leanne are amazing. I had many small businesses that need refinancing over the years. I have met many Brokers and there is always a catch. ALWAYS!… Use them! Once you do you will work with them forever

- Nirav Patel

If you searching for a great experience Commercial Loan Direct is the place. Leanne took care of me and honestly had the greatest experience. She handled all of my needs in a smooth and timely manner listened and addressed any concerns I had about the process and was very patient. I can be quite a handful at times and Leanne was so professional and kind hearted. I'd 100% recommend this company. Thank you again.

- Vincent Arias

We were in unfamiliar territory when it came to refinancing. Commercial Loan Direct streamlined the whole process for us. Leann connected us with lenders that were the right fit for us. The money and time we saved was so worth it. I highly recommend them

- Rita Pisarski

CLD Assistant

Online — Ready to help